Car accidents can have all kinds of adverse effects on people. Lack of oversight on your part may cause Prop 213 to come into play, and that can lead to some real problems. In certain situations, Proposition 213 could be the reason why you find yourself in a big financial hole you’re struggling to climb out of. If you were driving uninsured, Prop 213 may bar you from recovering non-economic damages like pain and suffering.

Saeedian Law Group has been handling car accident claims in California and beyond since 2009. Our team works closely with injured clients to build strong cases and fight for the compensation they deserve. Contact us today for the next best steps to take after a car accident in California.

So, what is Proposition 213, and does it apply to you? Those are some of the questions we’ll be addressing in this article.

What Is Proposition 213?

Proposition 213 may be something you’re not familiar with, but it’s been around for a long time. Officially, it’s known in California law as “The Personal Responsibility Act of 1996.” California voters adopted it at the November 1996 general election.

California Prop 213’s stated purposes are as follows. First, it notes that you should not reward uninsured motorists, drunk drivers, and felons for breaking the law. The proposition drew attention to “lawbreakers” recovering damages from law-abiding citizens due to the injuries they sustained because of the crimes they committed prior to the enactment of this law.

It also urged residents of California to make changes to the law so the individuals would not recover “unreasonable damages” from law-abiding citizens. Evidently, the appeals to the public worked, and they adopted the proposition.

In essence, Proposition 213 reduces the damages an individual can receive. It applies if they did not have insurance on the vehicle they drove at the time of the accident. The individual in question could still sue to recover certain damages, but there are restrictions placed on what they can ask for. The proposition effectively means that those who are insured can sue for more damages than those who aren’t.

When Does Proposition 213 Not Apply?

Here’s an important thing to note about prop 213. There’s a pretty good chance you’ll never need to worry about it if you’re always up to date with your insurance payments.

If you always make sure that you’re covered by insurance whenever you head out for a drive, the effects of the proposition are not going to have an impact on you. Since you are sufficiently insured, you can sue for everything the law entitles you to after a car accident.

Proposition 213 also has no effect on passengers involved in car accidents. It doesn’t matter whether the car you were riding in was or not. If you are hurt in the accident, you can file a lawsuit requesting both economic and non-economic damages.

We’ll get to what those economic and non-economic damages are a bit later in this article.

When Does Proposition 213 Apply?

We’ve now established that Prop 213 is nothing you need to worry about if you always have auto insurance and if you’re only a passenger in the vehicle. So, when exactly do you need to worry about the proposition affecting you?

It’s something you must keep in mind if you go out driving using an uninsured vehicle. Prop 213 applies when you were operating a motor vehicle that was uninsured, and you owned it. In that case, the vehicle involved in the crash had no valid coverage. About 20% of California drivers were uninsured in 2023, so this law reaches a lot of people.

Keep in mind that driving with no insurance is illegal in the state of California anyway. If you ever find yourself in the unfortunate position of being involved in an accident, the expectation is that you will be exchanging insurance information with your fellow driver.

Having no insurance puts the two of you in a more difficult situation, and it’s something Prop 213, and other laws are trying to prevent.

What Happens When Proposition 213 Takes Effect?

Like we noted earlier, there are restrictions placed on the amount of money you can sue for if Proposition 213 applies to your situation. To be more specific, the law will only permit you to sue for economic damages. You cannot recover non-economic losses, such as pain and suffering, unless an exception applies. These non-economic losses, sometimes written as noneconomic damages, stay off the table.

Are There Any Exceptions to Proposition 213?

Yes, some exceptions could come into play, which nullifies the effects of Prop 213. Let’s discuss them in greater detail below.

The Drunk Driver Exception

The first exception applies to incidents involving drunk drivers. Let’s say a drunk driver hit you while you were driving uninsured, leading to you getting injured. The law offers some leeway in that scenario. Under section 3333.4(c), this exception applies only if the at-fault driver is subsequently convicted of drunk driving. You’re not going to be penalized because of the drunk driver’s negligence. Instead, you will still be allowed to sue for both economic and non-economic damages stemming from the accident.

You Have Insurance for a Different Vehicle

You are also exempted from the effects of Proposition 213 if you have an auto insurance policy for a different vehicle. It’s possible you were only borrowing a car from your friend because yours was in the shop for repairs. Upon borrowing the car, you also may not have known that it was uninsured.

Because you have an insurance policy of your own, the law will still regard you as someone who’s insured. You can still file a lawsuit for all the damages you are entitled to.

The Uninsured Vehicle Belongs to Your Employer

Proposition 213 also does not apply if the uninsured vehicle you were driving belongs to your employer. Your employer may have some trouble recovering their losses, but the law will not get in the way of you receiving fair compensation.

Accidents That Occur on Private Property

The place where the accident occurred could also determine whether the proposition will apply. If it occurred on private property, then the proposition will likely not take effect.This is a fact-specific argument, not a settled exception. It rests on the idea that the financial responsibility laws require insurance to drive on public roads, not private ground.

The table below sums up when Prop 213 blocks non-economic damages and when an exception restores them.

| Exception Type | Description | Example Scenario |

| Drunk driver convicted | The at-fault driver is convicted of DUI | A drunk driver hits your uninsured car and is convicted |

| Own insurance on another car | You carry your own auto insurance policy | You borrow a friend’s uninsured car but insure your own |

| Employer’s vehicle | The uninsured vehicle belongs to your employer | You drive the company van, which the employer left uninsured |

| Private property | The crash happens off public roads | A collision in a private parking lot |

| No exception applies | You drove your own uninsured car | You are barred from non-economic damages |

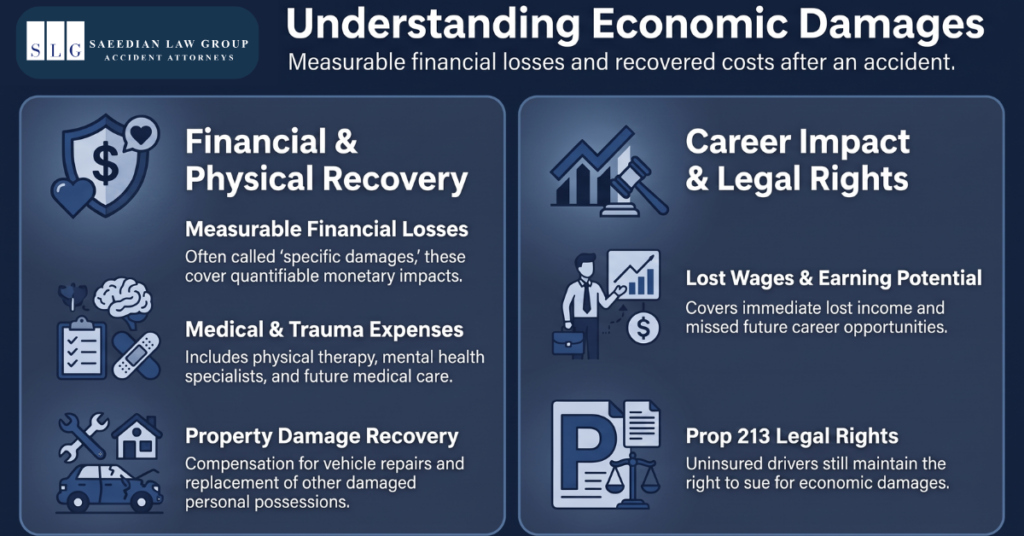

What Are Economic Damages?

We’ve been referring to economic and non-economic damages throughout this article. Now is a good time to discuss them in greater detail. Starting with economic damages, they constitute the compensation you can receive from measurable losses. They are also sometimes referred to as specific damages.

When we say economic damages, we’re referring to things such as your medical expenses. Those expenses may include the cost of physical therapy. If you must see a specialist due to the mental and/or emotional trauma you sustained because of the accident, they must cover the cost as well.

Future medical expenses for the lingering effects of your injuries may also be added to the calculations. In addition to your medical expenses, economic damages also account for potential property damage. The person who caused the accident must pay for the damage to your car, and any other possessions that were damaged.

Economic damages also include your lost wages. You probably cannot work if you sustained serious injuries from the accident. The economic damages will cover that.The law will also consider your earning potential when calculating economic damages. They will make calculations to account for the opportunities you missed out on due to your injuries.

Remember that Prop 213 does not prevent you from suing for the things mentioned in this section. Regardless of whether you had insurance at the time of the accident, you can still file a lawsuit in the hopes of receiving economic damages.

What Are Non-Economic Damages?

As you’ve probably guessed, the non-economic or general damages account for the losses that cannot be measured. Among the more common examples of non-economic damages are pain and suffering. Disabilities, disfigurement, and emotional distress are other items considered as non-economic damages.

In some lawsuits, the plaintiff may also claim that the accident led to the loss of enjoyment of life. They may also cite the loss of companionship as another reason why they are filing for non-economic damages.

Given that there are no concrete money figures to point to, calculating the non-economic damages in a case is a bit more complicated. Generally speaking, the non-economic damages rewarded in a case are related to the economic damages. Laws also cap the maximum amount of non-economic damages that they award.

Once again, it’s worth reiterating that Prop 213 prevents uninsured drivers from filing for non-economic damages unless they qualify for one of the previously noted exceptions.

How Proposition 213 Affects Settlement Offers and Your Legal Strategy

Prop 213 changes the math on a settlement. When the law bars your non-economic damages, insurance adjusters know your claim is worth less. They often open with a low settlement offer because your pain and suffering is off the table. An injured person who carried insurance can seek full compensation, including pain and suffering. Prop 213 limits non-economic damages, not punitive damages, which target a defendant’s misconduct.

That does not mean you should accept the first offer. Your economic damages, such as medical bills and lost income, can still add up fast. A careful review of those numbers often shows the first offer is too low. Michael Saeedian, the firm’s founding attorney, sees this often. “Adjusters treat a Prop 213 claim as a discount,” he says. “We push back by documenting every economic loss down to the receipt.” That paper trail is what moves an offer.

Tips for Maximizing Your Settlement despite Prop 213

Strong documentation is your best tool. These steps help protect the value of your claim. First, talk to a personal injury attorney early, before you speak with insurance adjusters. Second, document every economic loss, from medical expenses to replacement costs, with receipts and records. Third, explore whether a third party shares fault, since another responsible party can change your options. Careful preparation keeps the at-fault driver’s insurance from underpaying your claim.

Future Medical Expenses and Prop 213: What You Need to Know

Prop 213 limits your non-economic damages, but it does not touch your future medical costs. Future medical care is an economic damage, so you can still recover it even as an uninsured driver.

The challenge is proof. Future costs are easy for an insurer to dispute, so thorough medical documentation matters. A treating physician’s opinion on your long-term care needs helps establish the figure. Keep every record, because a well-supported claim for future medical expenses can be a significant portion of an uninsured driver’s recovery.

Why Do People Drive with No Insurance?

Considering all the potential complications of driving without insurance, ignoring that requirement is unwise. Even so, people still drive without insurance all the time. The possible explanations for why they continue with that practice are below.

High Cost

For many working people, having a car is essential to their daily routine. Without one, a trip that should only take about 15 to 20 minutes can extend all the way up to an hour. Knowing how difficult commuting can be, you will find people who will take out loans to purchase a car but skip on the insurance because they cannot afford it. Obviously, that is not a valid excuse for driving without insurance. However, it does reflect the reality that for many people, insurance is a necessity they cannot afford.

There’s no guarantee that you’ll find a workable insurance plan if you’re light on cash. The good news is that many agents are willing to work with drivers to find the plans that suit them best.

Unintentional Lapse

Another potential explanation for why someone is driving around with no insurance is because they weren’t aware that’s the case. Due to how busy you’ve been lately; you may have forgotten about the deadline for your insurance payment. Now, the coverage has lapsed, and you’re on the road without coverage.

Sadly, you may not realize that your coverage has expired until it’s too late. You may only realize your mistake when you’re exchanging insurance information with your fellow driver. By then, you may have already figured out that you’re in big trouble.

To avoid a costly mistake, always set up reminders for your plan. If you’re okay with setting up automated payments, then you can go for that option as well.

Lack of Understanding

Not everyone may be aware of the law mandating auto insurance. It’s not an excuse that will stick in court, but it could apply to some cases.

You may also find that some drivers are not willing to purchase insurance because they don’t understand how it benefits them. Teaching them more about the value of insurance could cause them to change their minds.

Overconfidence in One’s Driving Skills

The reason why someone refuses to buy auto insurance may also be because they believe they don’t need it. They may believe that they are good enough behind the wheel that they can avoid getting into any accidents while on the road.

While skilled drivers certainly have better odds of avoiding accidents, it’s still possible that another person on the road could cause them trouble. You can never be sure how your fellow drivers will move around you, so keep yourself covered by purchasing auto insurance.

Understanding Prop 213’s Legal Language and Codification

Prop 213 is not just a slogan. It became law and lives in the California Civil Code. You can read the exact language on the California Legislative Information site. The core rule sits in California Civil Code section 3333.4, which bars an uninsured owner or operator from recovering non-economic damages after a crash. A related section, 3333.3, bars a person from recovering any damages for injuries suffered while committing a felony.

In plain terms, the code turns the ballot measure into a hard limit on damages. If you drove your own uninsured car, the statute strips out your pain and suffering, no matter who caused the crash. Knowing the exact code section helps you and your attorney frame the claim correctly.

How Courts Interpret Prop 213 in Practice

California courts have shaped how far Prop 213 reaches. In Hodges v. Superior Court (1999), the California Supreme Court ruled that Prop 213 did not bar an uninsured driver’s product-defect claim against a carmaker. The court reasoned that a claim over a defective gas tank does not arise from the use of a motor vehicle. These rulings show the law is broad, but not unlimited. An experienced attorney reads them to find room for your recovery, such as a claim against a third party the statute does not cover.

How Can an Experienced Attorney Help You after a Prop 213 Accident?

It’s always in your best interest to work with an experienced attorney following an accident. For starters, your attorney can tell you what damages you can file for. They can tell you if you’re only qualified to receive economic damages or if you can include non-economic damages in your lawsuit as well.

A good attorney will also help you determine how much money to ask for in your lawsuit. Asking for an appropriate amount in your filing will increase the chances of the court ruling in your favor.

You also cannot discount the importance of having an attorney you can trust when you’re still dealing with the aftermath of the accident. Handling your legal affairs can prove to be a real challenge when you’re still hurting from your injuries. Entrusting those to your attorney is hugely important.

Whether or not Proposition 213 applies to your case, we at the Saeedian Law Group will do everything we can to ensure you receive the compensation you deserve. Call us today for a free consultation to learn more about how we can help.

Frequently Asked Questions

This section provides answers to common questions about Preposition 213.

What Does Prop 213 Mean in California?

Prop 213 is the Personal Responsibility Act of 1996. It bars uninsured drivers, drunk drivers, and felons from recovering non-economic damages, such as pain and suffering, after a car accident. They can still recover economic damages like medical bills.

Should I Accept the First Settlement Offer?

Usually not. A first offer is often low, especially when Prop 213 limits your non-economic damages. Have an attorney review your economic losses first. Accepting too early can leave real money on the table.

What Does Ruling Out Prop 213 Mean?

Ruling out Prop 213 means showing that the law does not apply to your case. It may not apply if an exception fits, such as a convicted drunk driver or your own insurance on another vehicle. If Prop 213 is ruled out, you can recover non-economic losses too.

What Are the Exceptions to Prop 213 in California?

The main exceptions include a drunk driver convicted of DUI and having your own insurance on a different vehicle. Others include driving an employer’s uninsured vehicle and some accidents on private property. Each can restore your right to non-economic damages.

Does Prop 213 Apply to Passengers?

No. Prop 213 does not limit passengers. If you are hurt as a passenger, you can seek compensation for both economic and non-economic damages, whether or not the vehicle was insured.

Disclaimer: The information on this website is provided for general informational purposes only and should not be considered legal advice. Reading this content or contacting Saeedian Law Group does not create an attorney-client relationship. Every case is unique, and past results do not guarantee future outcomes. You should consult with a qualified attorney to discuss the specific facts of your case before making any legal decisions.

Michael Saeedian founded Saeedian Law Group in 2009 with the goal of providing injured individuals and their loved ones with caring, personalized, and attentive legal representation.